How a Credit Dispute Affect Homebuyers Get an FHA Loan

This guide will cover how a credit dispute on a derogatory credit tradeline can halt the mortgage process on FHA loans. Millions of Americans fell victim to the economic, real estate, and banking collapse of 2008. The Great Recession of 2008 devastated more families than any other in U.S. history. Dale Elenteny of Non-QM Mortgage Brokers explains the Great Recession of 2008.

The Great Recession of 2008 was the longest-lasting Recession in U.S. history. Many experts consider it our second Great Depression and not a Recession. Bankruptcies hit historic highs. Countless hard-working Americans lost their businesses, jobs, pensions, and homes. The outcome of the real estate and credit meltdown left millions of Americans with bad credit. Credit repair companies started popping up out of nowhere. Many consumers turned to credit repair companies to fix their credit so they can qualify for a mortgage.

Countless folks who lost their homes and recovered signed up for credit repair programs so they could qualify for home loans. Borrowers do not need credit repair to qualify for mortgages. Credit dispute during the mortgage application process does more harm than good. Credit dispute on non-medical collections, late payments, charge-offs, and other derogatory credit is prohibited. This article will discuss and cover the dangers of credit disputes during the mortgage process.

Qualifying For an FHA Loan With Bad Credit

There are government and conventional loans for home buyers. The best loan program for home buyers with bad credit is FHA loans. The United States Department of Housing and Urban Development (HUD) is the Federal Housing Administration (FHA) parent. Alex Carlucci of Non-QM Mortgage Brokers explains the role of HUD on FHA loans:

HUD sets up FHA Guidelines. FHA is not a lender but a government agency that insures FHA loans. Banks and private mortgage companies originate and fund FHA loans. If FHA Approved Lenders follow HUD Guidelines when originating FHA loans. HUD will insure lenders on borrowers who default on their FHA loans.

The role of HUD is to promote homeownership to hard-working Americans with less-than-perfect credit with a 3.5% down payment. Credit repair is not necessary to qualify for FHA loans. Credit repair can do more damage than good during the mortgage application process. Credit disputes during the mortgage application process can disqualify many borrowers from qualifying for mortgage loans.

HUD Bad Credit Guidelines on FHA Loans

HUD understands that people can go through periods of bad credit. Many lost their businesses and jobs, which led them to bankruptcy and foreclosure due to the Great Recession of 2008. The 2008 financial crisis was the longest-lasting recession in U.S. history. It took over half a decade for a recovery, according to Mike Kortas, CEO of NEXA Mortgage, LLC.

The economic recovery took longer than most economic recoveries in history. Once Americans returned to work, many saw they had damaged credit.

Many hired credit repair companies to repair their credit and start re-establishing their credit. Other folks repaired their credit by themselves, hoping to delete prior derogatory information.

Basic Credit Repair Strategies To Get Approved For Mortgage

Anyone can repair their credit, and it is not rocket science to do credit repair. The way people repair credit is first to obtain a copy of the consumer credit report. The way consumers try to delete derogatory tradelines off their credit report is to dispute derogatory tradelines to the three credit reporting agencies:

How Credit Disputes Are Done

Consumers normally write them a letter disputing that the derogatory credit item is not theirs. Credit reporting agencies will contact the creditor consumers are disputing to verify the validity of the credit dispute. Zack Hoyer of Non-QM Mortgage Brokers is a credit repair expert and consultant. Here is how credit repair works, according to Zack:

If the creditor does not respond to the credit reporting agencies within 30 days, the credit disputed derogatory item needs to fall off the credit report. Credit repair companies use this strategy in repairing credit. However, this credit dispute strategy can backfire on consumers if they are in the mortgage application process.

There are many instances where retracting a credit dispute on the derogatory disputed item can backfire on the borrower and cause a mortgage loan denial. Retracting a credit dispute often drops credit scores.

Credit Dispute NOT Allowed During The Mortgage Process on FHA Loans

It will not matter whether mortgage applicants’ credit scores are over 800, but credit disputes on FHA loans on non-medical collections and derogatory tradelines are NOT ALLOWED.

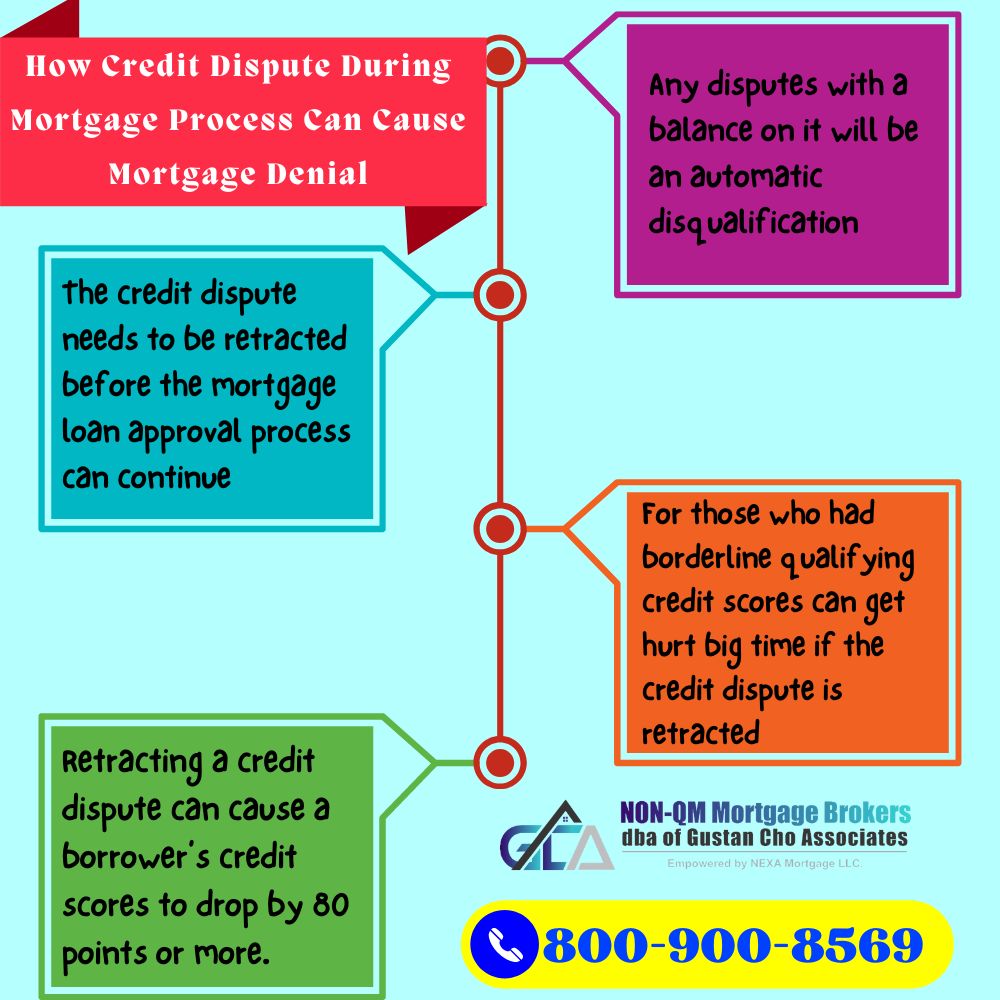

Any credit disputes on non-medical collections and derogatory credit tradelines with a balance during the mortgage process on FHA loans will be an automatic disqualification. The mortgage process will get halted until non-exempt credit disputes are removed. The credit dispute must be retracted before the approval of the mortgage loan.

Mortgage loan originators should not issue a pre-approval until they have reviewed the borrower’s credit report and made sure that there are no credit disputes on their credit report. Credit disputes can be retracted, but the major problem is that once a credit dispute is retracted from the borrower’s credit report, the borrower’s credit scores will drop. Those with borderline qualifying credit scores can get hurt if the credit dispute is retracted. Retracting a credit dispute can cause a borrower’s credit score to drop by 80 points or more.

Things To Consider Before Hiring a Credit Repair Company

Consumers planning on hiring a credit repair company and intending to buy a home soon tell credit repair companies that they do not want to dispute derogatory credit items with credit balances on them. Another thing consumers should realize is that older derogatory items stay on the credit reports for only seven years and have no impact on credit scores.

Many times consumers do not need the services of a credit repair company. The older the credit derogatory item is, the less impact it has on the consumer’s credit scores. Many times credit scores will not change by having a derogatory item deleted. Getting a recent late credit payment deleted via the credit dispute method is next to impossible.

The older the derogatory item is, the easier it is to remove it from the credit report. Homebuyers can still qualify for a mortgage approval with prior bad credit and outstanding collections and charge-offs without having to pay them off.

Why Lenders Do Not Allow Credit Disputes During The Mortgage Process on FHA Loans

Credit dispute on derogatory information is not allowed on FHA loans because the credit bureaus’ algorithm will negate the scoring system on disputed credit tradelines. Dale Elenteny of Non-QM Mortgage Brokers explains why credit tradelines on disputed credit tradelines increase:

Once a consumer disputes a negative item, such as a recent late payment, the credit bureaus automatically state the verbiage: Consumer disputes the credit tradelines. This verbiage automatically triggers the credit scoring system to remove the derogatory item from the formula. Consumer credit scores will automatically go up.

Credit scores increase on disputed credit tradelines because the derogatory item is non-existent in the scoring model. When consumers retract the credit dispute, the credit bureau scoring system will factor the derogatory item back into the scoring system, so the consumer credit scores will drop.

Importance of Removing Credit Dispute Before Issuing a Pre-Approval Letter

One of the major reasons for a mortgage loan denial is that loan officers issue pre-approval letters without carefully reviewing borrowers’ credit reports for any disputes. Borrowers go out and enter into a real estate purchase contract. Dale Elenteny of Non-QM Mortgage Brokers says a pre-approval letter should never get issued for a borrower with a credit dispute on a non-medical collection account or derogatory credit tradeline:

When their mortgage application process starts and the underwriter sees credit disputes, the loan is suspended until it is retracted.

Once the disputes are retracted, the borrowers’ credit scores can plummet, and they no longer qualify for a mortgage loan. Credit disputes on non-medical collections that are over 24 months old are exempt.

Credit Dispute Exempt From Retraction During The Mortgage Process

Certain credit disputes on FHA loans are exempt from retraction during the mortgage process. Medical collections are exempt from credit disputes. Non-medical collections with zero balances are exempt. Borrowers with outstanding non-medical collections under $1,000 are exempt from retracting credit disputes. Non-medical collections that are 24 months old or older are exempt.

If borrowers have credit disputes and the loan officer realizes they will not qualify for an FHA loan if disputes are retracted, the loan officer can request a manual underwrite without retracting the credit disputes.

Borrowers who need to qualify with a five-star national lender with no overlays on government or conventional loans can contact Non-QM Mortgage Brokers at 800-900-8569 or text us for faster response. Or mail us at gcho@gustancho.com. The team at Non-QM Mortgage Brokers is available seven days a week, evenings, weekends, and holidays.