Conditional Mortgage Approval From Underwriter

This guide will cover conditional mortgage approval from the mortgage underwriter during the home loan process. Once borrowers submit a mortgage loan application, it gets processed and submitted to underwriting. Once submitted to underwriting, it gets assigned to a mortgage underwriter. Fiona McCue, a senior mortgage processor at Non-QM Mortgage Brokers, explains the role of the mortgage underwriter as follows:

The mortgage underwriter’s job is to analyze and scrutinize every aspect of a mortgage application with a fine-tooth comb. The mortgage underwriter will go over income by not just checking off on W-2s and paycheck stubs. But will also go over tax returns to see if borrowers had any deductions

Non-QM Mortgage Brokers offer W-2 Income Only Mortgages where no tax returns are required. This is only offered to W-2 wage earners and is available on FHA, VA, and Conventional loans.

How Do Mortgage Underwriters Analyze Unreimbursed Business Expenses

Borrowers who deduct many expenses on tax returns will be deducted from monthly income calculations. The mortgage underwriter will also go over the credit report thoroughly and check the following:

- credit history

- any delinquencies

- collections

- public records

- bankruptcies

- foreclosures

- deed-in-lieu of foreclosures

- short sales

- judgments

- liens

- charge offs

- late payments

- available credit on revolving credit accounts

Once the mortgage underwriter feels borrowers qualify for a mortgage loan, the underwriter will issue a conditional mortgage approval.

What are the Conditions of Conditional Mortgage Approval?

In the following paragraphs, we will discuss clearing conditions on conditional loan approval by the mortgage underwriter.

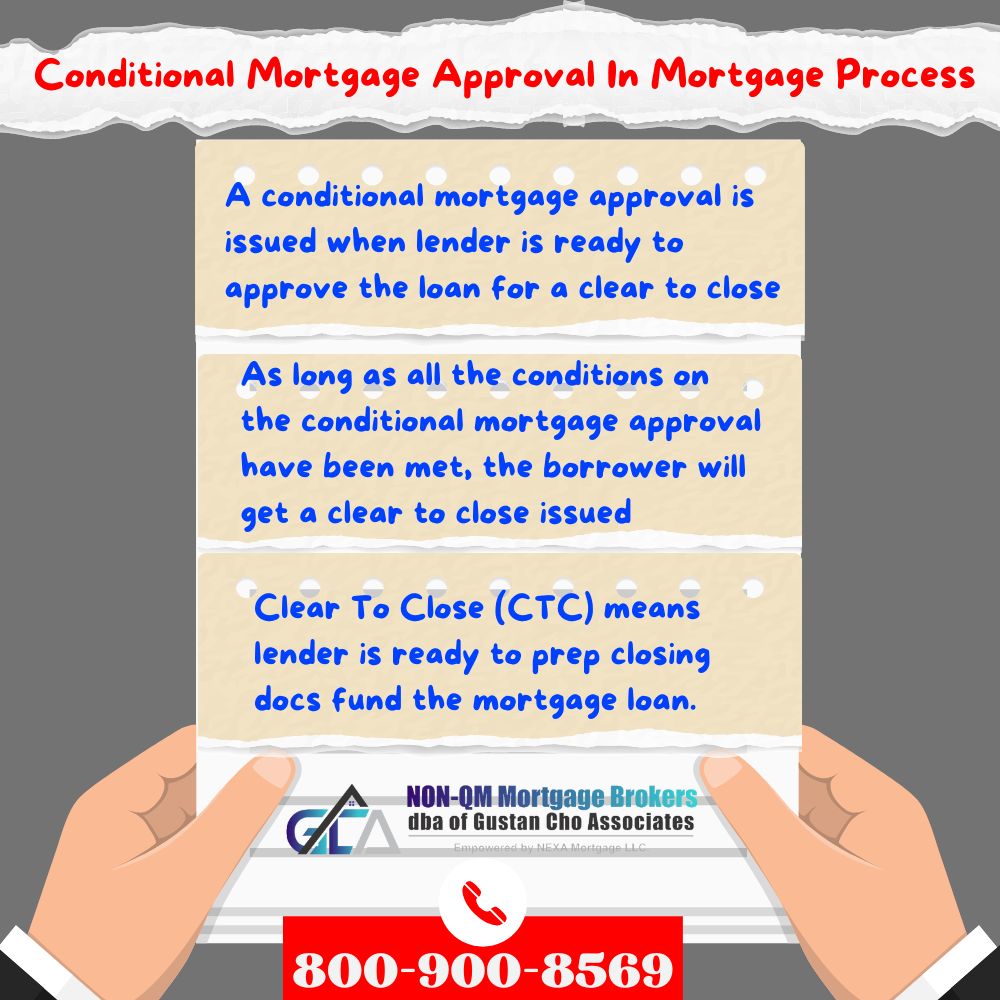

Just because the borrower gets a conditional mortgage approval does not mean the mortgage loan is ready to close. Conditional mortgage approval is issued when the lender is ready to approve the loan for a clear to close. This only holds as long as the conditional mortgage approval commitment conditions have been met. There may be one or two conditions, or I have seen as many as 50 or more conditions on a conditional mortgage approval. As long as all the conditions on the conditional mortgage approval have been met, the borrower gets clear to close issued. Clear To Close (CTC) means the lender is ready to prep closing docs to fund the mortgage loan.

The key to having as few conditions as possible on a conditional mortgage approval is to get the mortgage loan package as complete as possible before submitting it to underwriting. Many times, mortgage processors submit the mortgage package with missing information. This is because it was not provided to them by the borrowers.

Depending on the processor, he or she can submit the package with incomplete information and realize that the information not submitted will be a condition. This is normally a bad practice. For example, here is a case scenario. If the mortgage processor were to submit just one month’s bank statements and not the two months required, the mortgage underwriter would condition for the missing one month’s bank statements. To avoid getting a long list of conditions, the key is to provide a complete possible package to underwriting.

A good processor will even have letters of explanation from the mortgage loan borrowers in the original mortgage package. Bankruptcy And Foreclosure paperwork especially.

Clearing Conditions or Conditional Mortgage Approval

For example, an underwriter will issue a conditional mortgage approval on borrowers with prior bankruptcy, foreclosure, deed-in-lieu of foreclosure, or short sale. However, the mortgage underwriter will condition letters of explanation on why the mortgage loan applications filed bankruptcy or had a foreclosure, deed-in-lieu of foreclosure, or short sale.

A seasoned professional loan officer and processor will ask for this information before it gets submitted to underwriting. The same goes for credit inquiries which most people have. A mortgage underwriter will condition letters of explanation on credit inquiries after issuing the conditional mortgage approval.

Submitting the letter of explanation on the credit inquiries before submitting it to the underwriter will eliminate that condition. Do not be surprised to get conditional mortgage approval with 30 or more conditions. No need to panic

Examples of Conditions on Conditional Mortgage Approval

Conditions requested in a conditional mortgage approval may seem petty and ridiculous but need to provide the mortgage underwriter with what he or she is asking for.

Not all underwriters are created equal. There are mortgage underwriters that are super reasonable. Others will ask for the most insignificant item that sometimes does not make sense. Borrowers also need to understand the stress and financial responsibility mortgage underwriters have

One mistake from a mortgage underwriter can mean that the underwriter’s mortgage company cannot sell the mortgage loan they originate on the secondary market. A mortgage underwriter will get scrutinized if their approved mortgage loan falls into default. I can understand why mortgage underwriters are so anal regarding conditions.

Documents Requested By Underwriters

For example, when borrowers provide bank statements to mortgage underwriters, all pages need to be provided, including blank pages. One mortgage underwriter did not issue a clear to close because one of the blank pages did not have a page number. The blank page from the bank statement did not have a blank page number. Borrower got a letter of explanation from the banker stating that the blank page did not have a page number. The banker signed, stamped, and dated the letter and a new bank statement (No page number on the blank page), but the underwriter did not honor it. Fortunately, the file did get clear to close because the managing underwriter signed off on it. Cases like these can happen with conditions from conditional mortgage approval.

What Is a Clear To Close During The Mortgage Process

Once all the conditions have been turned in, the processor will review the submitted conditions. The processor will not submit parts and pieces of conditions. The processor will wait until all conditions have been met and satisfied and will then submit everything all at once

If the processor forgets to submit one or two conditions from the conditional mortgage approval list, the whole file will get kicked back. The whole file will go at the back of the line, which will then cause a delay in getting clear to close.

It is of major importance that the whole set of conditions gets submitted at once

Updated Mortgage Loan Approvals

In many instances, mortgage underwriters can issue new sets of conditions after the underwriter has issued an initial conditional mortgage approval.

What is mortgage underwriters’ discretion? Once the mortgage underwriter goes through the conditions that were requested, two things can happen. A clear-to-close is normally issued at this time. However, the mortgage underwriter can decide to attach another set of conditions.

When the mortgage underwriter adds more conditions and does not sign off on the original conditions list, it upsets everyone, especially borrowers. Some borrowers get extremely upset that they threaten the loan originator that they will go somewhere else.

There are cases where sellers threaten to retract the purchase contract when extensions are requested from the buyer’s side when additional conditions are requested from the mortgage underwriter. There is no way of fighting this. The best thing to do is do what the underwriter asks and get them the additional conditions as soon as possible so he or she can sign off on a clear to close.

How Long Does It Take For Underwriter To Review Conditions?

Sometimes, conditions get submitted to mortgage underwriters, and everyone waits for a clear to close. How long does it take for an underwriter to sign off on final conditions? Probably no more than 30 minutes. Unfortunately, even if all conditions are turned in, depending on the mortgage lender. Turnaround time can be 24 to 48 hours for the mortgage underwriter to sign off on the conditions and issue a clear to close.

Quality Control Process During The Mortgage Process

Most mortgage lenders have an underwriter who underwrites the mortgage loan and issue the clear to close. Once they receive all of the conditions from the conditional mortgage approval, they will issue a CTC.

Some Lenders Have Quality Control

However, there are some mortgage companies where once the mortgage underwriter signs off on the conditions, the whole mortgage package goes to QC. The Quality Control process normally takes 48 hours. What the QC underwriter does is the following:

- Re-review the whole file to make sure that there were no mistakes made

- QC will go over the appraisal

- might do a verbal verification of employment

- run a soft credit pull to make sure that the mortgage loan borrower did not incur more debt

- make sure the whole mortgage file is in compliance

- Once it passes QC, the mortgage loan is issued a clear to close

- Again, not all mortgage companies have Quality Control, but this process takes at least 48 hours or more for those that do.

Homebuyers and homeowners who need to qualify for a mortgage with a national direct lender with no mortgage overlays can contact us at Non- Qm Mortgage Brokers at 800-900-8569 or text us for a faster response. Or email us at gcho@gustancho.com. The Non- Qm Mortgage Brokers team is available seven days a week, evenings, weekends, and holidays.